Definition of Crypto Assets and Exclusion from Inventory

The Japanese Income Tax Act contains specific provisions related to cryptocurrencies. Since these provisions specifically target cryptocurrencies, the definition of the term “cryptocurrencies” is critical to determining when these rules apply. In this context, Article 2, Paragraph 1, Item 16 of the Income Tax Act, which defines inventory, stipulates the following:

For income tax purpose, inventories refer to goods, products, semi-finished products, work in progress, raw materials, and other assets (excluding securities, cryptocurrencies as prescribed in Article 48-2, Paragraph 1 of the Income Tax Act, and forests) related to a business generating business income, as specified by a Cabinet Order.”

Cryptocurrencies, as mentioned in Article 48-2, Paragraph 1, is defined according to the Payment Services Act. Therefore, Article 2, Paragraph 1, Item 16 clarifies that, concerning inventories, cryptocurrencies regulated by the Payment Services Act is excluded from being categorized as inventories for businesses generating business income.

Provisions regarding Inventories (for Domestic Consumption and Valuation Methods)

This provision suggests that, if not explicitly excluded, cryptocurrencies could potentially be classified as inventory. It also implies that, unless otherwise specified, the inventory-related provisions of the Income Tax Act do not apply to cryptocurrencies. For example, the following provisions are not applicable to cryptocurrencies:

- Article 39 of the Income Tax Act: This article states that the market value of inventories used for personal consumption by the business owner must be included in gross revenue when calculating business income, timber income, or miscellaneous income.

- Article 47 of the Income Tax Act: This provision outlines the methods for valuing ending inventories(year-end inventory) when calculating necessary expenses for business income. These methods, including specific identification, first-in, first-out, last purchase price, and lower-of-cost-or-market, do not apply to cryptocurrencies (Order for Enforcement of the Income Tax Act, Articles 99 and 99-2).

Regarding point 2, the Income Tax Act contains specific provisions on the valuation of cryptocurrencies, which will be addressed in a separate article.

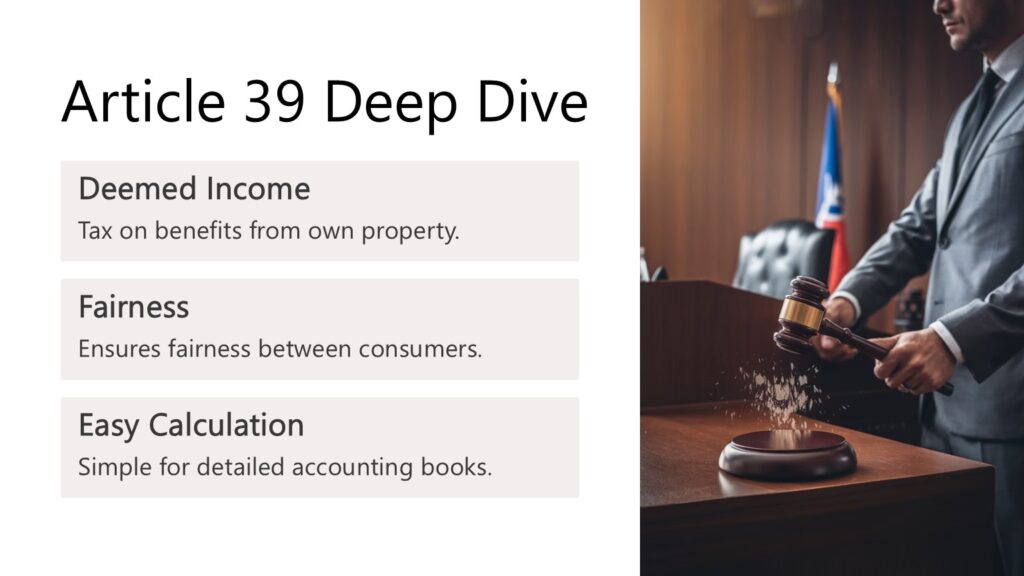

Now, we will examine Article 39 in more detail. Article 39 stipulates that where a resident consumes inventories (including assets specified by Cabinet Order as equivalent to inventories) for household use, or cuts and consumes timber for household use, the value of these assets at the time of consumption shall be included in gross revenue when calculating the business income, timber income, or miscellaneous income of the resident for the year in which the consumption occurs.

Note: The inventory subject to the above stipulation includes assets equivalent to inventory related to activities that generate real property income, timber income, or miscellaneous income, as well as certain small depreciable assets or lump-sum depreciable assets that are not essential to the business (Order for Enforcement of the Income Tax Act, Articles 81 and 86).

In practice, the market price or normal sales price is typically used to determine the value. However, if the business operator records an amount that is at least 70% of the normal sales price and no lower than the acquisition cost, this amount can be used as gross revenue for business income calculations (Basic Directive on the Income Tax Act, 39-1, 39-2).

This provision effectively means that even in the absence of actual income from external transactions, tax will be imposed on deemed income—economic benefits gained from one’s own property or labor. It has been suggested that Article 39 was introduced to address the following concerns (see Hiroshi Kaneko, “The Structure of the Income Concept in Tax Law,” in Studies in the Income Concept, pp. 89 et seq., Yuhikaku, 1995):

• Taxing imputed income from personal consumption of inventories ensures fairness between consumers who purchase goods at market prices.

• For business owners maintaining detailed accounting books, calculating imputed income is straightforward, making taxation on such income relatively simple.

• In certain cases, the amount of imputed income can be substantial.

Currently, cryptocurrencies are primarily used as a means of payment, exchange, or investment, and it is rarely regarded as having specific practical uses or as something that diminishes through consumption.

Given this, there seems to be little need to apply Article 39 of the Income Tax Act to cryptocurrencies.

Exclusion from Fixed Asset Definition

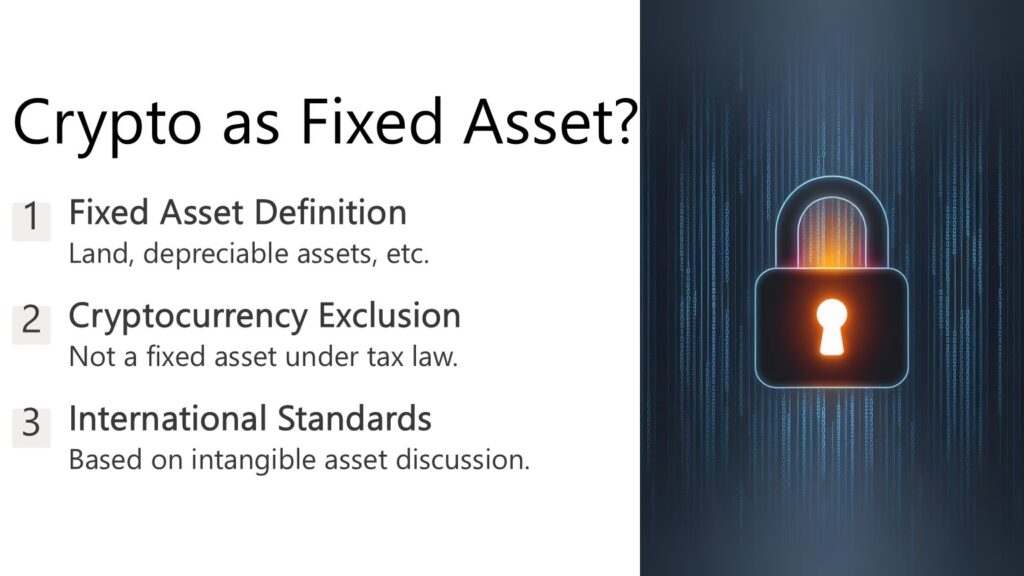

Fixed assets, as defined by the Income Tax Act, include land (including any right on land ), depreciable assets, telephone subscription rights, and other assets, excluding forests, as prescribed by a Cabinet Order.

The Cabinet Order clarifies that, among assets other than inventories, cryptocurrencies under the Payment Services Act, securities, and deferred assets are excluded from being categorized as fixed assets (Article 2, Paragraph 1, Item 18 of the Income Tax Act, Article 5 of the Order for Enforcement of the Income Tax Act).

Similarly, under the Corporate Tax Act, cryptocurrency is also excluded from the definition of fixed assets (Article 2, Paragraph 1, Item 20 of the Corporate Tax Act, Article 12 of the Order for Enforcement of the Corporation Tax Act). This exclusion is based on the International Accounting Standards Board’s discussion of whether virtual currencies should be classified as intangible assets (see Ministry of Finance, “2019 Tax Reform Commentary,” p. 290). Although the term ” virtual currencies ” was updated to “crypto asset” under the 2019 revision of the Payment Services Act, for the purposes of this article, we will continue to use the term “cryptocurrencies” for convenience.

Definition of Cryptocurrency under the Payment Services Act

Finally, the Payment Services Act defines “crypto asset” as follows:

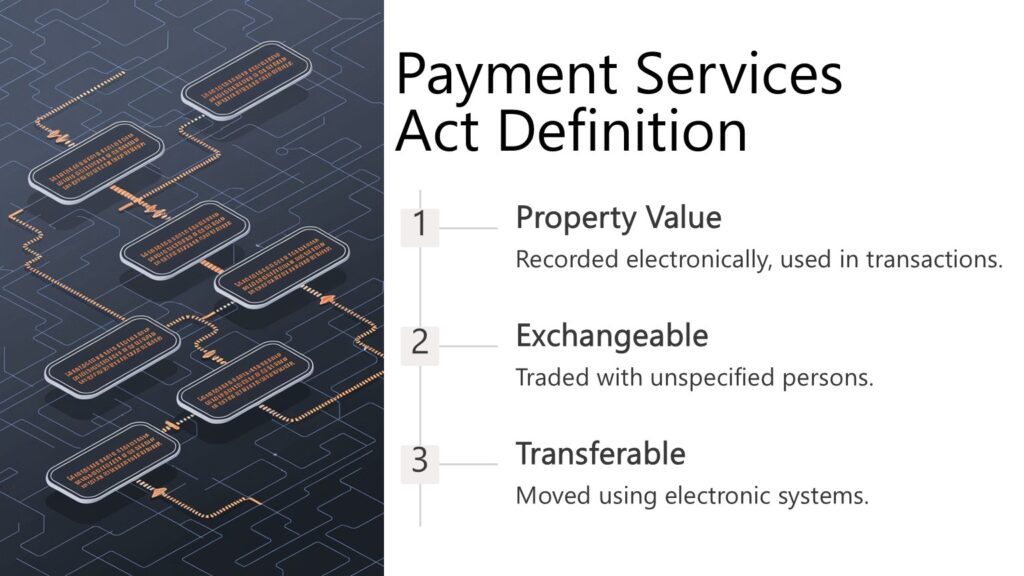

“A ‘crypto asset’ under this Act refers to any of the following, excluding those indicating rights prescribed in Article 29-2, Paragraph 1, Item (viii) of the Financial Instruments and Exchange Act:

- Property value, limited to that recorded on an electronic device or by electronic means (excluding Japanese currency, foreign currencies, currency-denominated assets, and electronic payment instruments, except those categorized as currency-denominated assets), which can be used in transactions with unspecified persons for the purchase or leasing of goods, or the provision of services, and can also be bought, sold, and transferred using an electronic data processing system.

- Property value that can be mutually exchanged with the item mentioned above, with unspecified persons acting as counterparties, and transferred using an electronic data processing system.